The MSCI global share market index has had a volatile ride in 2022, falling 13.8% from its highs before rebounding 10.0% as at close of business on the 4th of April. What has driven this volatility? The initial weakness was driven in part from a sharp turnaround in policy direction from central banks to focus upon tackling inflation. This led markets to price in higher interest rates. In NZ and the US market pricing is for cash rates to rise 1.9% and 2.3% over the next year to 2.9% and 2.6% respectively. This has the impact of making shares less attractive on a relative basis and in time slowing growth and therefore company profits – a clear negative for share markets. The fall in shares was compounded by uncertainty around the Ukraine war and the resulting large increase in energy prices. Higher energy prices are effectively a tax on consumers and are likely to lead to slower growth and higher inflation.

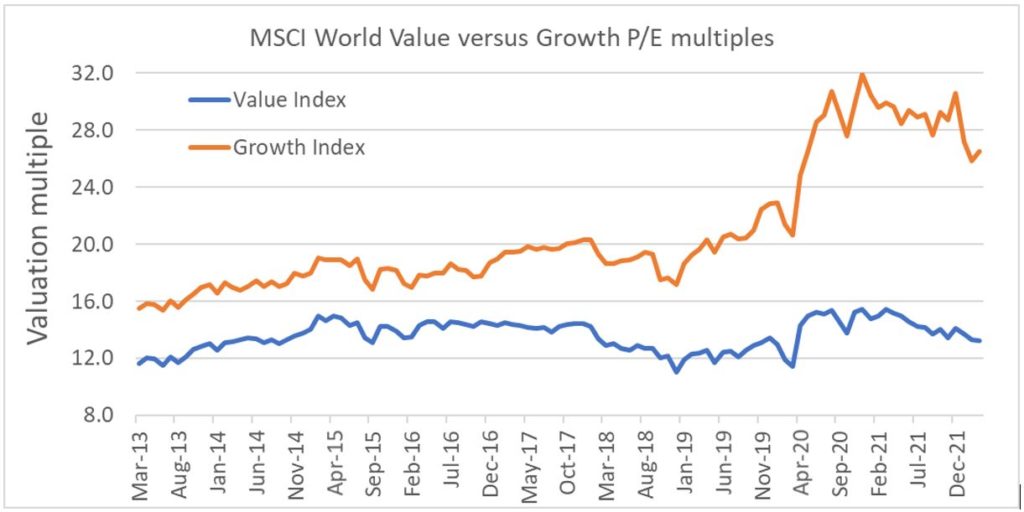

What is more difficult to explain is the recent sharp rebound in global share markets and company valuations against what remains a highly uncertain backdrop. Generally, in times of uncertainty, investors demand higher returns and therefore lower valuations. Part of the rally in share markets we suspect has been due to strong demand from retail investors who are more focused upon strong historic returns and market momentum and less on valuation and future returns prospects. The valuation of the MSCI global growth share market index, often favoured by retail investors, remains high. However, the valuation of the global value market index which includes less exciting companies, such as banks and energy companies, remains around long-term averages.

Source: MSCI – https://www.msci.com/

At Milford we continue to believe that this valuation dispersion creates a good environment for company selection and added value. We continue to focus upon those companies which are benefiting from the current environment and are attractively valued. This includes the agricultural equipment manufacturers; John Deere, Agco (maker of Massey Fergusson) and CNHI (maker of Case and New Holland). Agricultural commodity prices such as wheat have risen approximately 33% year to date as the market looks to diversify supply away from Russia and Ukraine. So whilst we remain cautious on the broader outlook for share markets, there remains plenty of companies that we believe offer good medium-term risk adjusted return prospects.