UK Supermarkets: Stable not Sexy

The UK grocery market is one of the most competitive in the world. With four “full choice” supermarkets – Tesco, Sainbury’s, Asda and Morrisons – this market was already highly competitive before the European discount operator Aldi and Lidl entered the market in the mid 1990s. Since then, Aldi and Lidl have grown their market shares to nearly 20%, pressuring the sales and margins of the four large incumbents.

On face value, such an industry doesn’t make for an appealing investment proposition. The two listed supermarkets, Tesco and Sainbury’s, are delivering sales growth of 3-4% and profit margins (defined as earnings before interest and tax over sales) of less than 5%. However, the defensive nature of these cashflows, tailwinds such as increased at-home dining, and successful strategies enabling share gains, have proved appealing to investors. The share prices of Tesco and Sainsbury’s increased 29% and 28% respectively in 2025.

Sainsbury’s Plc – Winning Share and Driving Growth

Sainsbury’s is the UK’s second-largest supermarket, serving more than 19 million customers a week across approximately 600 supermarkets and more than 800 convenience stores.

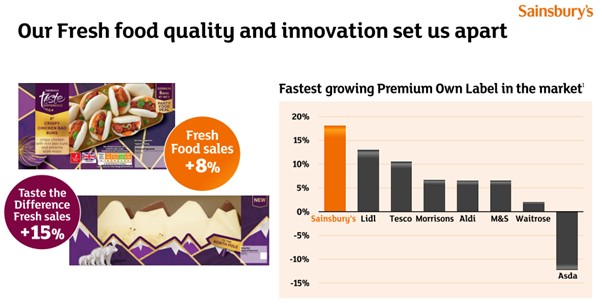

At its core, the business is built on a “Food First” strategy, competing on combination of value, quality, and service. As well as delivering low prices via its “Aldi price match”, ensuring it is competitive with the low cost supermarkets on every-day food items, the business is focused on lifting innovation and quality via its own brand “Taste The Difference” range, which is appealing to consumers switching from restaurants and take-aways. Its loyalty programme called “Nectar” is one of the UK’s largest, and this isn’t just about points; it’s a data goldmine. By using machine learning to offer 500 million personalised offers per week, Sainsbury’s is offering value and driving repeat purchases, while generating high-margin revenue through its retail media agency, Nectar360.

The strategy of value, quality and service has allowed Sainbury’s to grow sales and market share consistently for more than two years, with its share of the UK grocery market now approaching 15%. It is attracting more customers, and more “big weekly shops” via its expanded value and range. In addition, it is opening 40 new stores to increase the geographic areas it serves away from its roots in the south of England. This scale is being combined with investment in its existing store network and distribution network to help Sainsbury’s cut costs and improve margins. This is enabling reinvestment in prices and quality, further driving share gains. This virtuous cycle of cash returns is a boon for shareholders; it expects to return over £800 million to shareholders through a combination of dividends and a share buyback in the 2025/26 financial year.

Source: Sainsbury’s Q3 Trading Statement presentation, January 2026

A divided investment case

Despite its 2025 share price performance, investors remain divided on Sainsbury’s investment case, as evidenced by the level of short interest in the stock. If the supermarket business is the jewel in the crown, Argos is the chink in the armour.

Argos, a general merchandise retailer with a history as a paper catalogue business, has struggled in the face of competition from Amazon and a weak UK retail environment. While Sainsbury’s has closed physical Argos stores, reduced costs and restructured its offer to be more competitive, it is a small drag to Sainsbury’s group profit and potentially a distraction to management. However, this is both an opportunity as well as a threat. Sainsbury’s management team is executing a turnaround plan that could lead to profitability over the next two years, or the ability to sell Argos and distribute the proceeds to shareholders. Investors are watching the performance of this business closely.

Stable, not sexy

While supermarkets don’t make for very exciting investments; stable business models that can deliver defensive cashflows are an important part of diversified portfolios. Recent share market volatility has increased the relative attractiveness of these types of investments, and while this has reduced the returns on offer via good share price performance, we continue to look for businesses that have low risk, pay attractive income returns, and have the opportunity to drive share price performance via delivering earnings ahead of investor expectations. Sainsbury’s could do this via continued share gains in its core supermarket business and the turnaround of Argos.