Investment markets move up and down – this volatility is an expected part of investing. We appreciate that trusting the investment process can be challenging at times. However, as an investor, you should be wary of reacting to headlines and before making any major changes, be sure to ask yourself if your investment objectives have changed or if you are simply feeling nervous due to news you’re hearing.

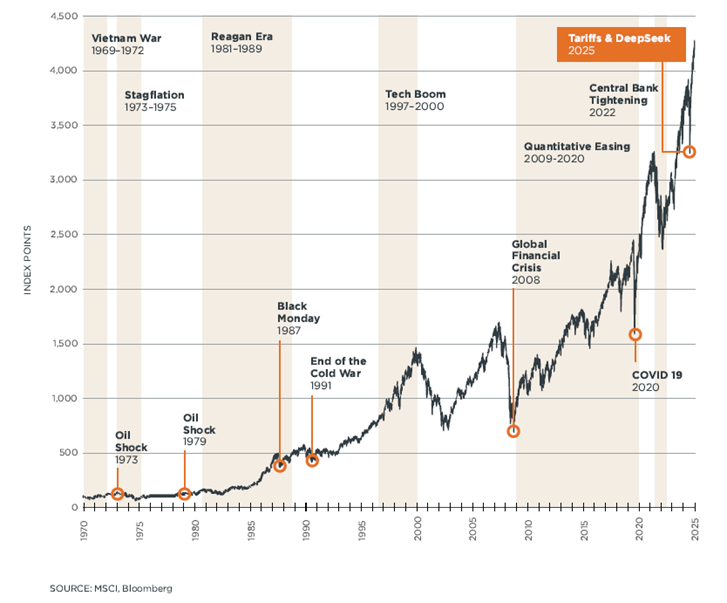

Markets have weathered Middle East crises before, and the record is reassuring. Looking back at the significant market downturns over the past three decades, the pattern is consistent: market downturns tend to be temporary, recoveries have followed, and those who have stayed the course and remained invested have been rewarded. The consistent lesson: geopolitical shocks cause real short-term pain but rarely derail long-term returns.

Long-term view of investment markets since 1970

While the value of your investment can rise and fall in the short term, over longer periods markets tend to rise overall, and we encourage you to remain focused on your long-term investment goals. If your goal is to fund your retirement that is decades away, a short-term dip in markets and your KiwiSaver balance today is unlikely to affect your end result.

One of the most effective buffers against volatility is holding a broad mix of investments across asset classes and sectors, so when one area comes under pressure, others can cushion the impact. Milford's funds spread exposure across equities, fixed income, property, and cash funds across New Zealand and global markets, so you're not dependent on any single market to deliver your long-term returns.

When volatility rises, it can be tempting to "do something" by switching into more conservatively positioned funds or moving to cash. The problem is that these decisions often lock in losses after prices have already fallen - and then investors can miss the sharp rebounds that frequently occur when conditions stabilise. Missing just a handful of the market's strongest recovery days can materially reduce long-term outcomes.

Continuing to make regular contributions to your investments when markets dip means that you are able to buy more units with your money because the unit price is lower. For example, if you contribute $80 a fortnight, you could buy 8 units when the unit price is $10, but if the unit price falls to $8 you would then be able to buy 10 units. Over time, if you continue to invest regularly, you will buy units at many different prices, and this is known as 'dollar cost averaging'. If you stop contributing when markets fall, you will miss out on the benefit of being able to buy more units for your money when the price is cheaper, or 'on sale'. This is why you often hear investors talk about "buying the dip".

We want to reassure you that our investment team are constantly assessing the market and analysing data, to help us make informed decisions on the best places to invest your money. Our ability to move quickly means we can take advantage of opportunities as they arise and manage risk along the way. Our use of specialised tools, known as derivatives, can also help cushion the effects of large downward market movements. Our focus remains on delivering strong long-term investment performance.

If you are anxious about your investment, financial advice may help. Financial advice can help you understand your risk tolerance and ensure you are in the right fund for you. We have a KiwiSaver Digital Advice tool available, or you can get in touch and speak with a Milford Financial Adviser.

For more information and to see our Financial Advice Provider Disclosure statement, please visit our milfordasset.com/getting-advice.