It’s hard to believe what has happened in the last few months: the declaration of a global pandemic, an oil price crisis, markets falling drastically from February all-time highs, and trillions of dollars of stimulus promised by policy makers around the world.

As investors, identifying safe-haven investments available in Australia has been challenging, particularly with growing uncertainty about how long our economy will be in hibernation. Historically, one safe haven option has been gold. Gold has traditionally been viewed as a portfolio diversifier, but recent moves have been more correlated with equity markets. Australian gold miners initially declined significantly as the COVID-19 selloff began. In this article we explore why we consider gold a portfolio protector, and how we are getting exposure in our portfolios.

Why do investors hold gold in the first place?

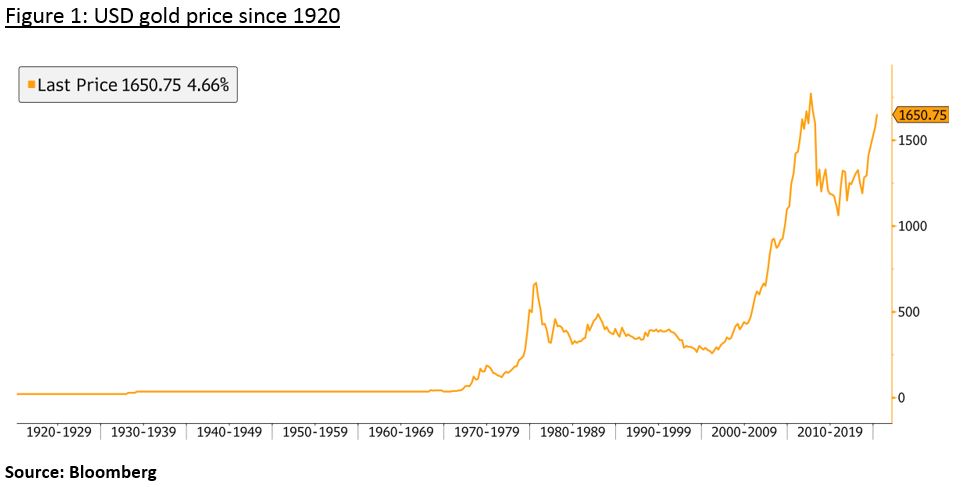

- Gold has increased in value against all currencies over the long-term. During a debasement of currencies as a result of monetary policy, or inflation from fiscal policy, gold typically appreciates in value. Figure 1 shows the gold price in US Dollars since 1920. The period up to 1973 is when the US Dollar was pegged to gold. Despite this period of stability, gold has appreciated in USD at 4.66% per annum since 1920.

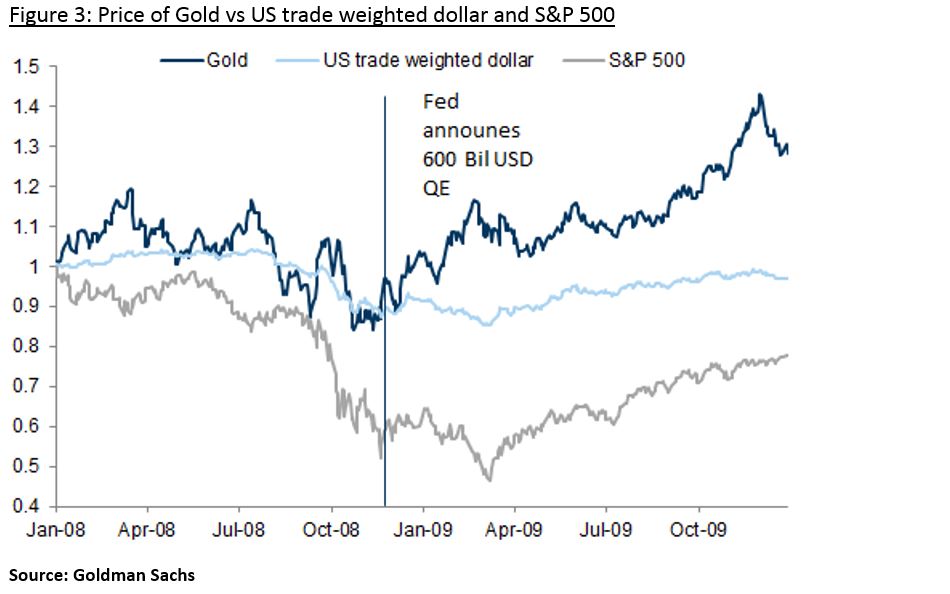

2. Gold can also be used as a diversifier in portfolios, as more often than not it moves inversely to share markets. The caveat to this it that during times of severe market stress gold miners can decline despite a robust gold price (Fig.2).

Why does the price of gold fall in a crisis?

In a crisis, gold can sell off with equities as funding constraints cause investors to sell liquid assets (like gold) to create liquidity. Large falls in the price of oil has exacerbated this sell off as it has created US dollar shortages for Emerging Market countries. This has driven up the value of the US dollar and put pressure on the gold price in US dollars. We have seen this relationship between equity markets and gold before in 2008 until the Fed stepped in with QE in November 2008.

Is now the right time to buy gold?

With the US Federal Reserve locking itself in to “infinite QE” and the US Government providing a historic US$2.2 trillion of stimulus, gold is likely to appreciate. If this fiscal spending creates inflation, then gold is likely to increase a significant amount. Even with no obvious headline inflation, because the demand shock offsets printed money, gold still likely appreciates against the US dollar and other currencies given the large increases in supply. Despite recent volatility in the price of gold, we still believe that gold is a currency of last resort and negative interest rates reduces the opportunity cost of holding gold.

How can investors get exposure to gold in their portfolios?

There are many ways that you can get exposure to gold as an investor. The most common ones include:

- Physical gold

- ETFs of physical gold

- Gold mining companies

Within the Milford Australian Absolute Growth Fund and Milford Dynamic Fund our preference is to hold gold mining companies given our focus on owning direct equities. Mining companies can offer a leveraged play on the gold price and can also generate an income stream, unlike physical gold which you must pay to store and generates no income.

Gold mining companies still hold physical gold but act as a leveraged play on the gold price given the margin between their costs of production and the gold price. Companies have the potential benefit of increasing production through more efficient mining or finding new deposits.

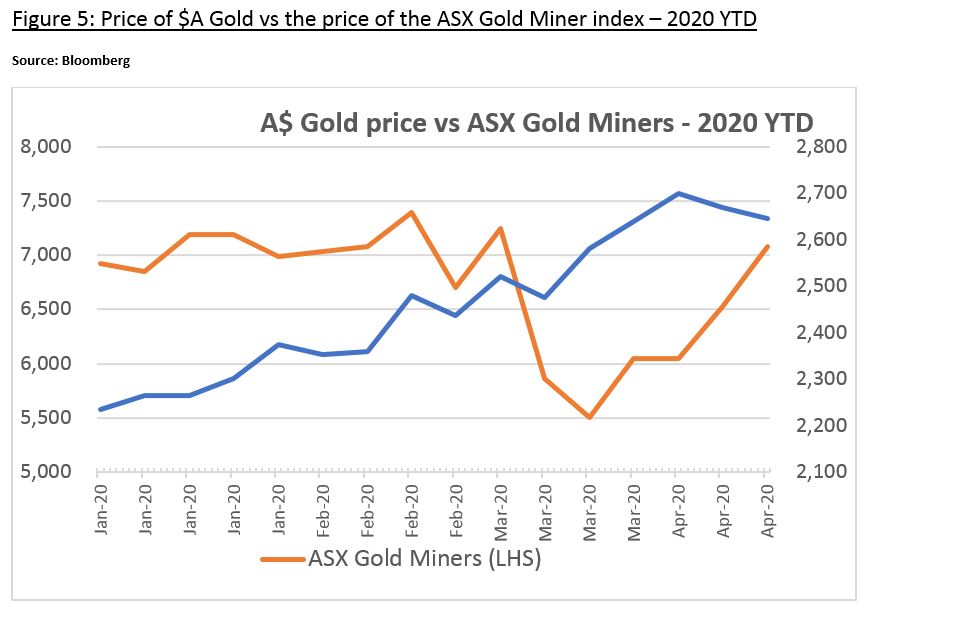

An investment strategy that focuses on doing fundamental research on mining companies, in our view, can earn a higher return than physical gold, albeit with higher volatility in the short-term. As shown in Fig.5, gold miners have underperformed physical gold during the recent sell off representing a good opportunity to invest. It should be noted that there is some risk in the short-term that gold miners underperform if COVID-19 causes mining activities to be curtailed.

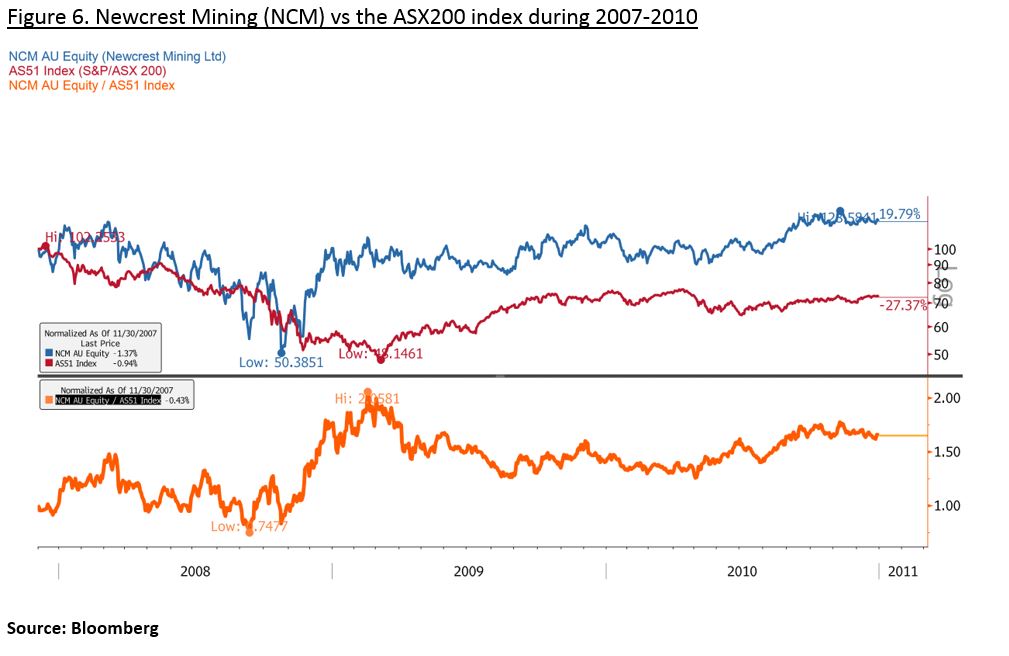

Despite higher relative risk than physical gold, direct equity mining exposure can still be beneficial for portfolio diversification and overall returns. This is illustrated by the Fig.6 below that highlights the absolute and relative performance of a gold mining company vs the ASX200 index during 2007-2010.

What are the risks to our thesis?

- Gold could continue to be a source of liquidity and put downward pressure of its price

- 51% of demand for gold is still jewellery and this demand could fall if we head into a global recession

- 8% of gold demand in recent times has been net central bank purchases, mainly from emerging countries. These countries may have to sell gold to raise US Dollars.

- Speculative net long gold futures have declined by about a third but remain somewhat elevated. This could decline further.

- Mining companies face production shutdown if workers are infected with COVID-19 or governments force them to do so as a precaution

Despite the recent volatility in gold prices and correlation to equity markets we fundamentally think that having exposure to gold in portfolios will act as a hedge against inflation and currency debasement. Although the performance of gold miners may be volatile in the short-term, the monetary and fiscal response to the COVID-19 pandemic is ultimately very positive for these companies.

Milford Australia Gold Exposure:

| Gold exposure as at 31/3/2020 | Milford Australian Absolute Growth Fund | Milford Dynamic Fund (Small Companies) |

| Total portfolio exposure to gold miners | 10.9% | 10.7% |