Written by Ryan Williams, Senior Analyst

Global energy policy is rapidly evolving, particularly de-carbonisation targets in Europe which have been accelerated with the goal of creating energy independence in response to the Russia-Ukraine war. These policies in Europe may extend to other developed countries and are expected to significantly disrupt the current investment landscape for energy creating “winners” and “losers” as the energy mix shifts.

European Policy

On 18th May 2022 the European Commission released its “RePowerEU: Affordable, Secure and Sustainable Energy for Europe” plan which was backed by the 27 European Environment ministers in late June. The new plan is a direct response to Russia’s invasion of Ukraine: “The RePowerEU plan sets out a series of measures to rapidly reduce dependence on Russian fossil fuels and fast forward the green transition, while increasing the resilience of the EU-wide energy system”.

Short-term measures to immediately reduce reliance on Russian fossil fuels include2:

- Common purchases of gas, LNG and hydrogen via the EU Energy Platform

- New energy partnerships with reliable suppliers, including future cooperation on renewables and low carbon gases

- Rapid roll out of solar and wind energy projects, combined with renewable hydrogen deployment

- Increased production of biomethane

- Approval of the first EU-wide hydrogen projects in the coming months

In addition, some key medium-term measures were introduced that are targeted to be completed before 20273 :

- New national RePowerEU Plans under the modified Recovery and Resilience Fund – to support investment and reforms worth €300 billion

- Boosting industrial decarbonisation with €3 billion of frontloaded projects

- New legislation and recommendations for faster permitting of renewables

- Investments in an integrated and adapted gas and electricity infrastructure network

- Increase in the European renewables target for 2030 from 40% to 45%

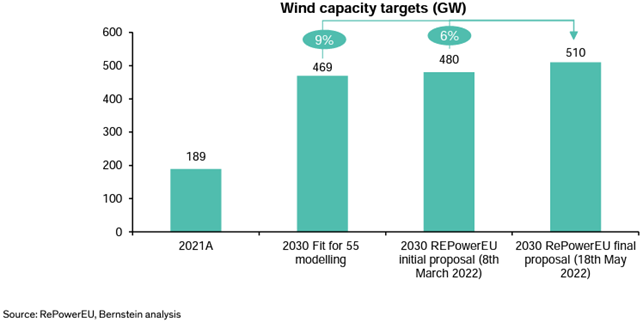

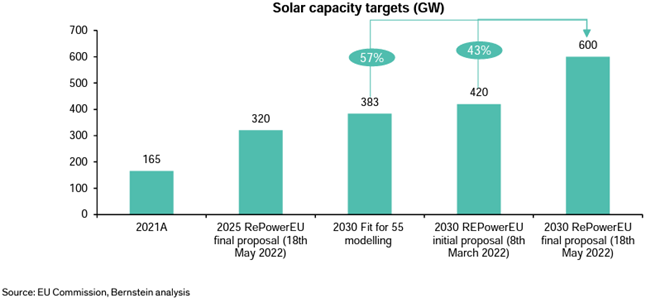

Specifically, these targets include significant increases to solar and wind production targets (even compared to targets set earlier in 2022)4:

In addition to renewable generation targets, the EU is also looking to reduce emissions by changing usage behaviours. These include energy efficiency targets as well as a law requiring new cars sold in the EU to emit zero CO2 from 2035 , making it impossible to sell internal-combustion engine cars from 20355.

The policy targets and goals announced by Europe may extend to other developed markets, with groups such as the G7 stating the importance of “increasing energy security through an accelerated energy transition”. The policy landscape requires close attention when it comes to energy.

What does all this mean for our investments?

Energy producers have been attractive income vehicles for many years as they are stable, regulated businesses with strong cashflow generation. As regulation and policy changes there will likely be “winners” and “losers”. Within the universe of Global Real Assets investments several investment sectors will be impacted including: Independent Power Producers and Regulated Power Utilities (both conventional and renewable producers), high speed rail and airports, pipelines, toll roads, and others.

Renewable energy companies (both regulated and independent power producers) will need to make significant investments in renewable energy projects to meet government and corporate emissions targets. These investments will include technologies that are already proven to produce energy at scale such as wind (offshore and onshore) and solar, as well as new technologies such as renewable hydrogen.

As the energy transition accelerates the “winners” and “losers” will become clearer, but it is likely to be the case that the companies who are already well on their way to transitioning to renewable energy will be well placed given their experience and capability in delivering through this rapidly evolving landscape.

Going forward we must carefully consider how the current European policy response (which is primarily led by energy independence) might lead to policy changes in other countries. We must also consider how these policy changes will affect the adoption of new technologies and how this might impact individual companies and our investments.

References:

2. https://ec.europa.eu/commission/presscorner/detail/en/fs_22_3133

3. https://ec.europa.eu/commission/presscorner/detail/en/fs_22_3133

4. Bernstein European Renewables: RePowerEU Accelerating renewable and Green Hydrogen deployment May 2022

5. https://www.reuters.com/business/autos-transportation/eu-lawmakers-support-effective-ban-new-fossil-fuel-cars-2035-2022-06-08/