Much has been written about the so called Great Intergenerational Wealth Transfer and rightly so, because this constitutes the largest redistribution of wealth in human history. To summarise what this means; in most developed countries (and particularly in New Zealand and Australia), a substantial portion of overall wealth is held by individuals born between the end of World War II and the mid-sixties (the so called “baby boomers”). Clearly a large proportion of the assets currently held by individuals in that age bracket will pass to their heirs over the next 20 – 30 years.

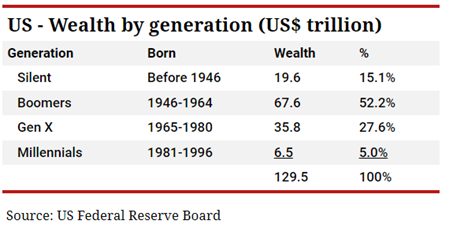

For example, see these figures from the US;

Of course, it’s not quite as simple as saying the wealth will pass straight from the “boomers” to the “Gen X / Millenials”. There are many factors affecting the quantum and timing of this transfer. For example, people are living longer and this costs money! Many of the boomer generation will want to retain a significant part of their wealth to ensure they have sufficient to cover long term old age care costs and a large part of their asset base may be taken up by those costs. Others will want to retain and maybe spend their accumulated wealth – perhaps they don’t want to leave a “nest-egg” for the next generation! Different dynamics within each family will also affect the transfer (for example, an increasing proportion of families have complicated dynamics caused by blended families, divorce, disagreements within families and so on, which adds to the complexity of wealth transfer). Finally, many will want to bequeath some assets to charity as part of the transfer process.*

Despite the diluting effect of the above factors, we can say for certain that a significant sum of assets will be passed between generations over the coming years, and it will be interesting to see how the next generation deals with this transfer. The different generations view wealth differently and these behaviours will have a big effect on how these assets are handled.

How to prepare

Many families find it difficult to talk about money, but it’s important to get over this initial hurdle and normalise these kinds of discussions because the outcomes are so much better if there is a plan involving future generations in place. This doesn’t have to be driven by the older generations of a family, if you’re in the younger generations you can also initiate these conversations and start to break down the barriers around meaningful financial discussions.

In addition to the obvious measures like ensuring your Will is up to date, create the opportunity to talk about the family values, how the family wealth is currently invested and why it is allocated in those areas. You may find you need to encourage the younger generations to educate themselves (or seek advice) on investment and strategies to protect the family wealth (or perhaps even the other way around and it’s the parents who should be encouraged to seek advice).

If you have a financial adviser, perhaps take the younger generations along to your next meeting to help them gain a full understanding of the management of the family wealth and their role in it.

Great financial advisers should have the technology to help model and visualise your financial goals, ensuring you have a clear idea of whether you can achieve them. Sometimes, simply testing a few scenarios can help solidify a plan for the future and increase your sense of comfort that what you have is enough.

*A final word on gifting to charity.

Sadly, the great wealth transfer described here is likely to exacerbate societal and economic inequalities in the developed world as the families of those baby boomers who didn’t quite make it onto the property ladder or who missed out on the other opportunities for wealth creation during that period will struggle to compete with those families that were fortunate enough to benefit. The “have-nots” will fall further and further behind the “haves”. It is therefore so important now more than ever, that the fortunate ones recognise this and put something back into communities that are struggling.

It’s often difficult to know where to start with such plans of giving. The Milford Foundation has been set up to help find prudently managed and impactful ways of making a difference.

For further information please go to www.milfordfoundation.co.nz