The investment implications of the war in Ukraine are considerable and it is difficult to appreciate the full extent of its impacts. We will lay out some of the clearer and immediate implications below from the point of view that conflict and hence economic sanctions against Russia are ongoing for the foreseeable future. A fast resolution to the conflict would of course change the situation and reverse many of the impacts discussed.

Most of the implications are due to the significant economic sanctions placed on Russia which effectively remove the world’s 11th largest economy and one of the world’s largest commodity exporters from the global economy. Some of the implications are due to Ukraine itself being a large exporter of certain commodities, as well as the uncertainty created by a conflict of this magnitude in Europe involving a nuclear armed nation.

1. Higher commodity prices and inflation

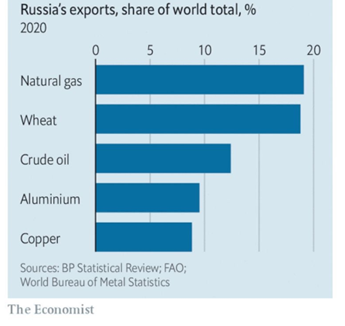

Russia exports 12% of the world’s crude oil and just under 10% of metals such as aluminum, copper, and nickel. It also exports 18% of the world’s wheat with Ukraine exporting another 11% meaning the two countries account for nearly a third of the world’s international wheat trade. Europe is particularly affected as it sources roughly 40% of its natural gas from Russia, mostly through pipelines into northern Europe.

Source: The Economist

Direct economic sanctions from the US and Europe will cover metals and hard commodities but are not yet aimed at disrupting the more sensitive flow of energy and food commodities from Russia (although the US and UK are now looking to sanction some Russian oil). Despite this, the supply of these important energy and food commodities is being disrupted for several reasons:

- SWIFT removal: the removal of some Russian banks from the SWIFT international banking network means commodity trading companies and banks either cannot settle transactions with Russian exporters or are unwilling to for fear of losing money.

- Self-sanctioning: there is a lot of “self-sanctioning” occurring where companies do not want to source commodities and goods from Russia for their own ethical reasons.

- Trapped ships: many shipments of goods simply cannot get to market as Russian ships are not welcome at international ports or the ships are trapped in the Black Sea due to the military conflict.

- Russia banning exports: more recently it looks like Russia may voluntarily ban exports of commodities for a period. This would be a retaliatory action to hurt the West.

As a result, commodity prices are surging.

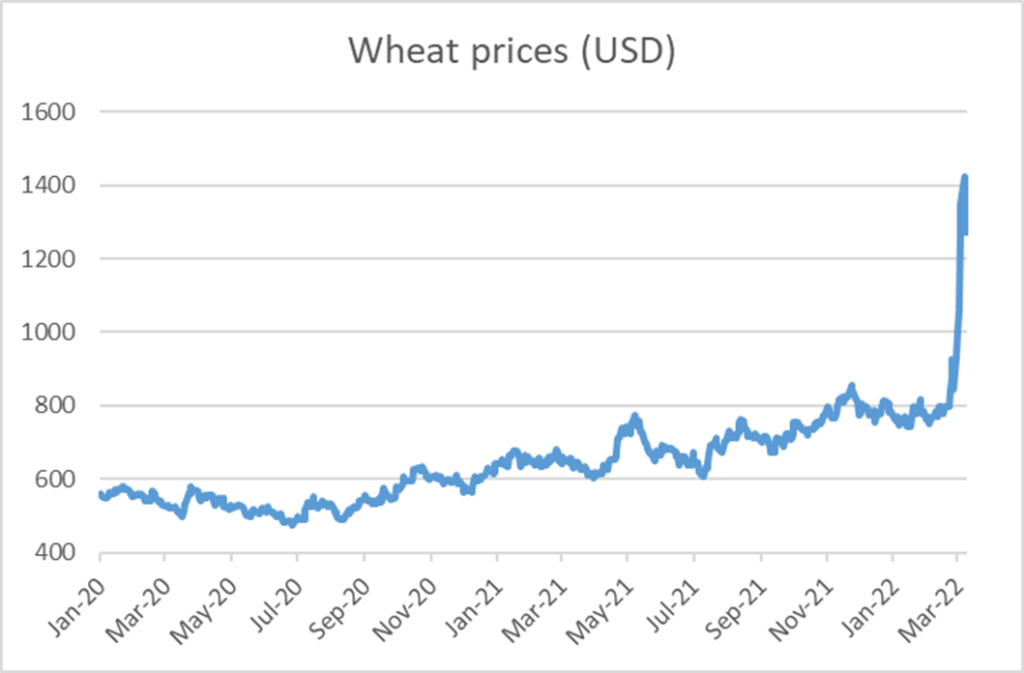

Wheat prices are up 50% since the conflict began and are now up 160% over the past two years. This is dragging up other agricultural commodity prices as the market anticipates substitution of wheat and changing eating habits.

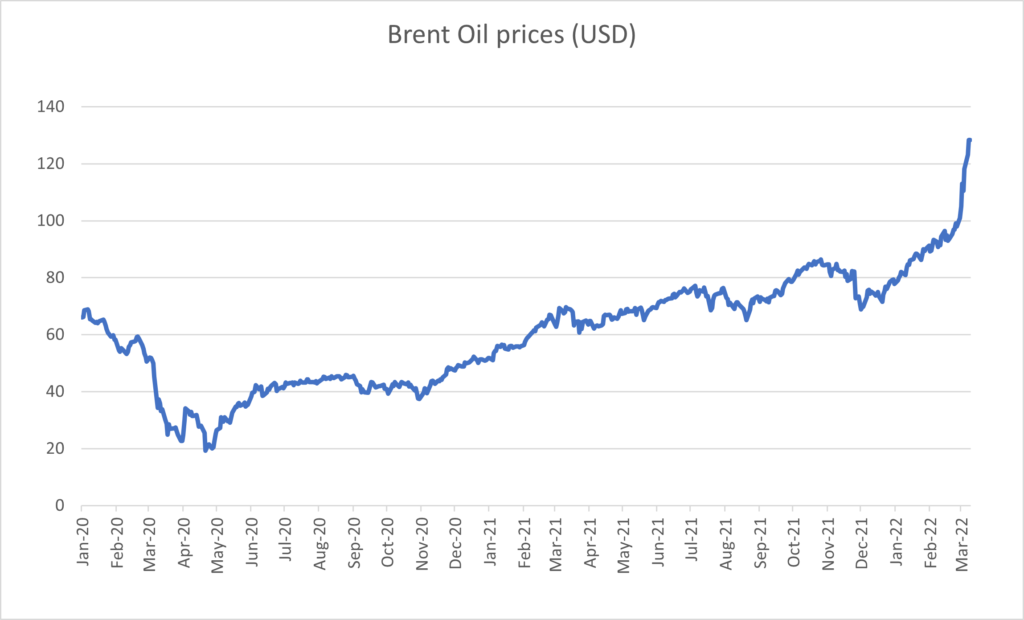

The oil price has traded as high as US$130 a barrel, up 60% since a month before the conflict, while most other commodities such as copper, nickel and steel are up sharply also.

Source: Bloomberg

Source: Bloomberg

This is going to exacerbate already high inflation that is increasing the essential cost of living for many countries around the world and causing more cost pressures for a lot of businesses. It is particularly bad for consumers as essential items of food and energy are experiencing the largest increases in price.

Eventually most of Russia’s metal exports will find their way to China as will much of Russia’s oil. This may partially alleviate some of the shortages we will see over the next couple of months. But either way you look at it, we will have commodity shortages while this conflict continues and higher prices unless an economic recession destroys demand.

2. Economic growth

High inflation and an absence of free Government stimulus cheques were always going to make a more challenging environment for consumers in 2022. The surging commodity prices, and uncertainty of conflict are likely to contribute to even more consumer weakness. This will be a drag on overall economic growth and profits of non-essential retailers.

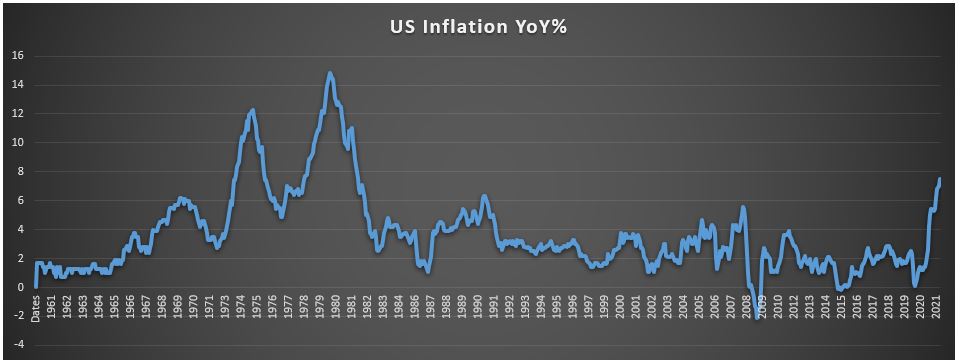

Largest inflation pressures since 1980

Source: Bloomberg

3. Challenges for central banks

Most global central banks have either begun to increase interest rates or are poised to begin a significant rate hiking cycle. This is aimed at slowing demand to bring inflation under control as price pressures prove larger and more persistent than central bankers expected.

Now we face a situation where inflation pressures will be even larger in the near term and economic growth is likely to weaken. Raising interest rates will help dampen inflation to some extent, but it achieves this buy reducing demand which puts even more downward pressure on economic growth.

Faced with this difficult situation it is not certain exactly what central bankers will do, however our base case is they still need to put interest rates up in the near term but may not raise rates as far in the medium term.

What does all this mean for our investments?

Commodity producers are well placed, and we have plenty of those in our portfolios – mostly Australian resource companies. These resources companies are a great addition to portfolios as their earnings will benefit as higher commodity prices cause all sorts of problems for many other businesses and broader markets.

Slowing economic growth leads to a more cautious view on other economically sensitive companies such as retailers and some financials. Owning more defensive companies makes sense if economic growth slows substantially.

It is possible we will see fewer interest rate rises this year from central banks which should eventually support valuations on the share market (compared to where they may have gone). To what extent risk aversion offsets this is unknown, but it certainly may help soften the blow of any economic weakness.

As mentioned earlier, this can all change if we are fortunate enough to get an end to the conflict and removal of sanctions against Russia. How that may occur and how likely it is is beyond the scope of this blog but the possibility is factored into our investment decisions. We are certainly not going “all in” on the investment strategy above due to the probability of a fast reversal.

This year was always going to be a year where active management of your investments was important. The Ukraine conflict only increases the importance of active management.