Freightways (FRW) is a leading operator of time-sensitive parcel delivery services in New Zealand and Australia. It operates several brands, from premium (NZ Couriers) to less time-sensitive services such as Post Haste, Castle Parcels and Now. Alongside temperature-controlled logistics brand Big Chill, this makes up the NZ Express Package segment of the business.

Freightways has also expanded into the much larger Australian market through the acquisition of Allied Express (a nonstandard-sized package courier business aka ‘ugly freight’) and another acquisition of VTFE, a Business-to-Business (B2B) express freight provider. This sets a great footprint for further expansion into the Australian market.

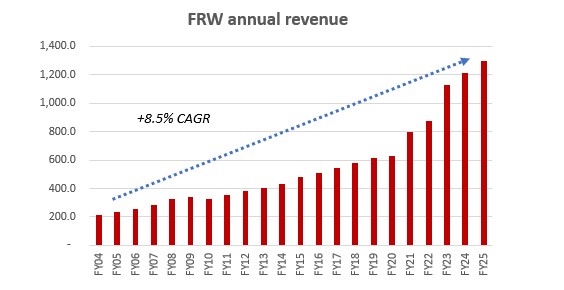

Source: Bloomberg, Milford analysis

New Zealand cyclical recovery

Part of the Freightways investment case centres on a return to attractive and sustained earnings growth in the NZ Express Package (NZEP) segment. This is driven by multiple levers including a recovering local New Zealand economy, market share gains, and improvements in margin expansion from more rationale local pricing and facilities utilisation.

Freightways has been delivering on many of these initiatives in recent years, especially continued improvements in same customer volumes vs the previous year. The Iranian situation and subsequent energy cost crunch may have delayed the local NZ cyclical recovery but, in our view, this will return. There was demonstrable evidence of better economic performance locally in the latter part of 2025 and early 2026.

Australian growth story

Another leg to our investment case is the impressive growth, both organic and inorganic, in Freightways’ Australian segment. In 2022, Freightways acquired Allied Express and, more recently, a further acquisition in 2025 of VT Freight Express.

The volume growth organically has been impressive in Australia since the Allied Express acquisition. This has been driven by a strong customer proposition, exposure to key pockets of the superior recent economic growth across the Tasman, and completion of several automation projects. The Australia business unit currently operates primarily in eastern seaboard main centres, and there remains a logical extension into deeper geographies throughout the country.

Mergers and Acquisitions (M&A)

Adding value through M&A, (especially into overseas geographies) can make many investors nervous, but we believe Freightways has delivered well on its acquisitions to date. It has remained patient, disciplined and has been very capital efficient in its decisions to date.

We expect Freightways to continue to pursue opportunities in the Australian market. It has previously stated it is seeking businesses in a variety of price ranges, some of which can be funded on balance sheet. Other larger M&A could require equity, which we believe would be well supported by the market given Freightways’ previous track record.

Outlook

We believe Freightways is well positioned to grow in the medium term. We see meaningful revenue growth linked to higher volumes on a local macroeconomic recovery, further Australian expansion, and continued market share gains. Larger scale, pricing initiatives and better utilisation of current facilities also give scope for margin expansion into the future.

The track record of delivering returns above cost of capital, disciplined execution on M&A, and strong aligned management makes Freightways a core holding across several Milford Funds.